Tweet of the week

PJT Summer Analysts:

|

|

|

|

|

Click Above to Access Content

|

|

|

|

|

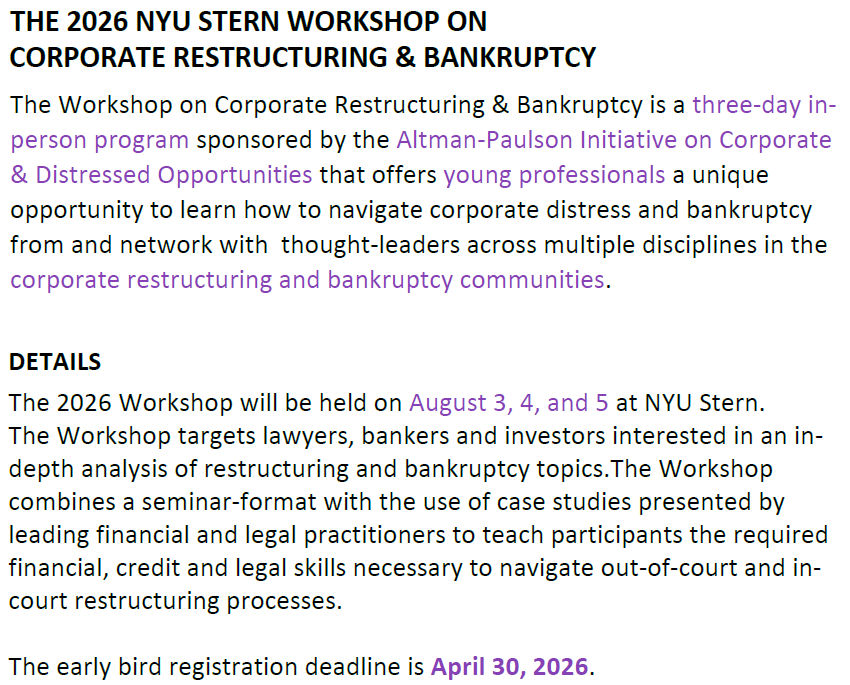

Featured Event

|

|

$100 off for CRC Subscribers!

Early Bird Ends April 30

|

|

|

|

| Learn More |

|

Click above to access content

|

|

CRC Subscribers Receive An Additional $100 off by emailing info@creditorcoalition.org

|

|

|

|

|

Exclusive Content

|

|

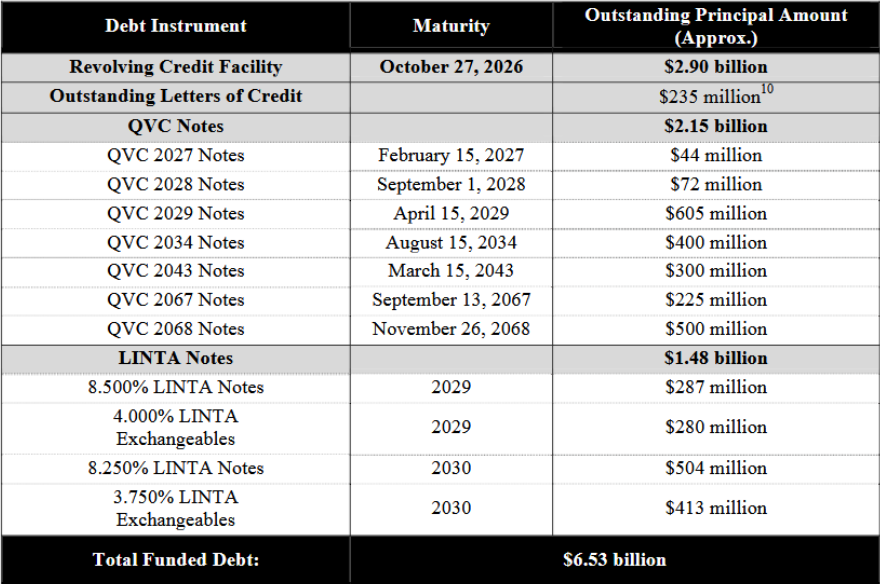

QVC cuts $6.6bn debt to $1.3bn

|

|

|

|

|

Click above to access content

One-time registration required

|

|

|

|

|

Exclusive Content

|

|

the end of a great story

|

|

|

|

Click above to access content

|

|

Our Take:

Multi-Color’s global settlement marks the end of an entertaining and equally significant bankruptcy proceeding. While we applaud the outcome, we question the means -- using a sitting judge to both mediate and adjudicate the same case undermines the integrity of the adversarial process. just saying...

|

|

|

|

|

Exclusive Content

|

|

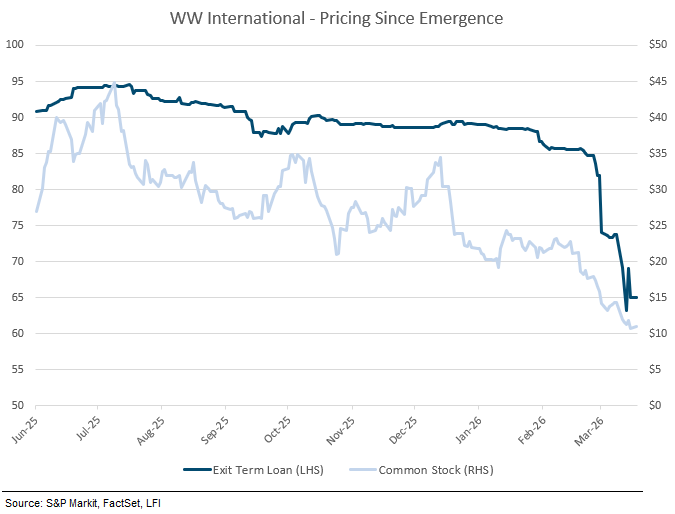

Exit TL slimming down @ 65c!

|

|

|

|

Click above to access content

One-time registration required

|

|

Our Take:

Nearly a year ago, WW International filed an eight-week prepackaged Chapter 11. First-lien lenders recovered roughly ~45 cents after marking post-reorg equity. We’ve since seen this playbook proliferate, as aggressive lenders and sponsors push RSAs through coercive distressed exchanges and the like. These prepacks, however, are mere financial engineering - a pseudo-extension of "in-court LMEs". The familiar “bad balance sheet, good business” narrative underpinning many RSA-driven prepacks has not held up in cases like Rite Aid, Spirit Airlines, and Party City. When — not if — WW returns for a Chapter 22, the real question won’t be capital structure, but whether there’s a business left worth restructuring at all...

|

|

|

|

|

In the news

|

|

Spirit going down the trash heap...

|

|

|

Click above to access content

|

|

|

|

|

Data Download

|

|

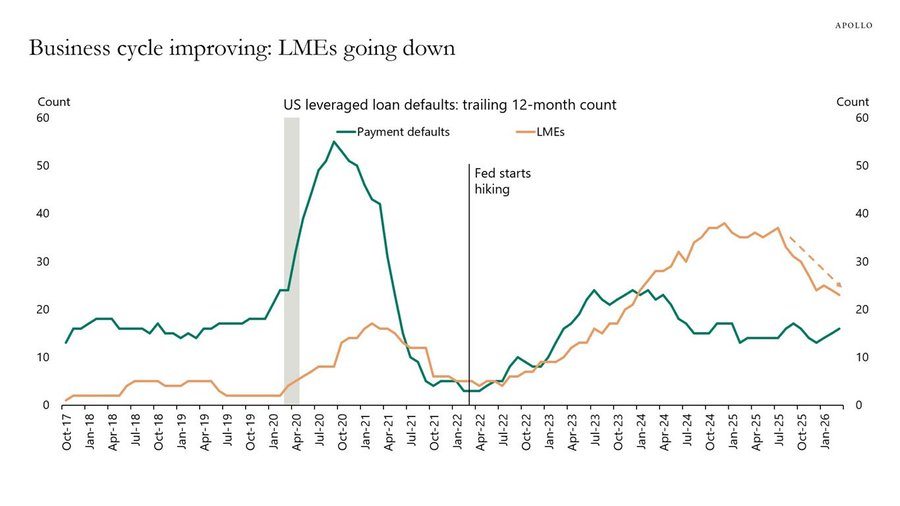

are we seeing a slow-down in LMEs?

|

|

|

Click above to access content

|

|

|

|

|

Exclusive Content

|

|

Driving straight into an LME...

|

|

|

|

Click above to access content

One-time registration required

|

|

|

|

|

Exclusive Content

|

|

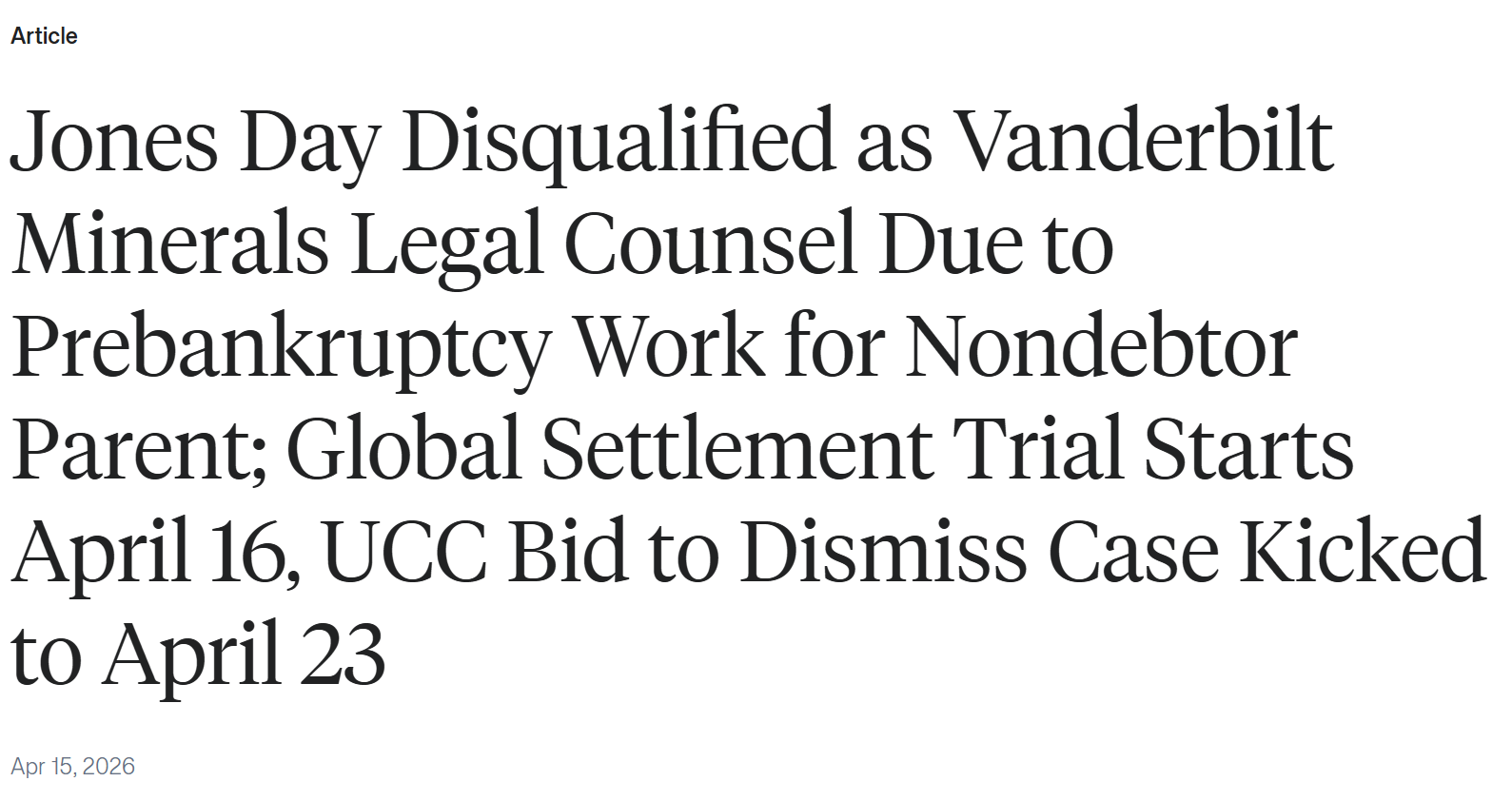

Jones Day makes the DQ list!

|

|

|

|

Click above to access content

|

|

Our Take:

It’s easy to forget, in an era of mega-bankruptcies and rockstar lawyers rotating among firms like a roulette wheel, that representing multiple clients—such as sponsors and their portfolio companies—risks the red card in the game of thrones.

|

|

|

|

|

Exclusive Content

|

|

LMT Primer Updated

|

|

|

Click above to access content

One-time registration required

|

|

|

|

|

Exclusive Content

|

|

an important issue waiting for its time

|

|

|

|

Click above to access content

One-time registration required

|

|

|

|

|

Featured Content

|

|

|

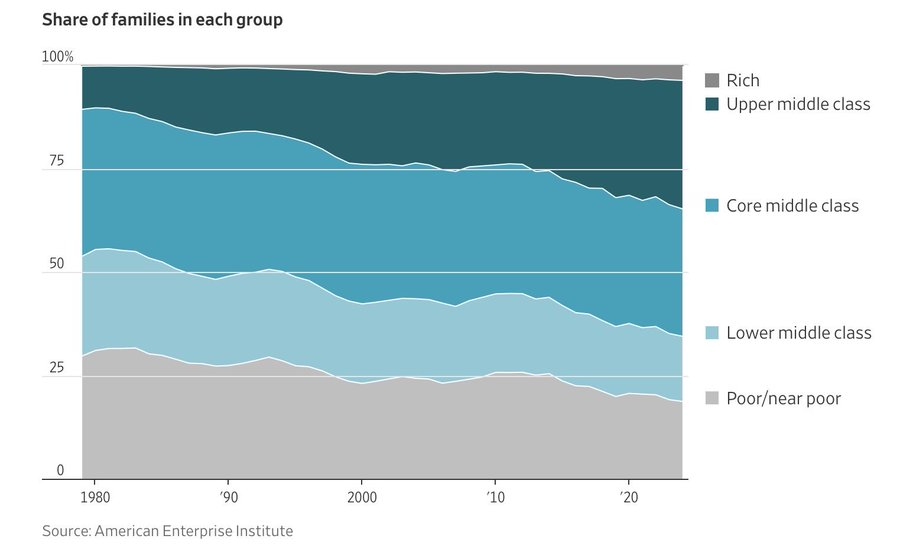

Consumer Sentiment is Stronger Than Reported

The University of Michigan Consumer Sentiment Index is widely followed as a key data point for gauging consumer confidence. In the latest survey, the index fell from 53.3 to 47.6, the lowest number ever recorded over its 70 years of history. The April 2026 report is worse than any single month since 1960, which captures 8 recession, periods of stagflation and the GFC.

Confused?

MainStreet Media reports this survey on the basis of its accuracy. I believe the survey is highly flawed, not close to providing an accurate portrayal, despite higher gas prices currently at the pump. Today, there is no recession, most consumers are doing relatively well with near full employment, and consumer net worth is near record levels.

This survey is likely biased towards lower income households or those with heavy partisanship, and furthermore it is statistically insignificant since it captures the opinions of only 900 households.

The below chart shows that the poor/lower middle class population has declined by 15% since the 1980’s (despite income disparity). The middle class/upper middle class segment has gained ground, lifting 15% of the population into its ranks; with households that have now accumulated greater wealth.

Takeaway: investors should remain vigilant on sectors of the economy that rely on low income households, which this survey captures, such as low-FICO consumer loans and related ABS.

|

|

|

Click above to access content

To follow Bruce's thoughts on the markets, investing and more, follow

@bruce_markets

|

|

|

|

|

Exclusive Content

|

|

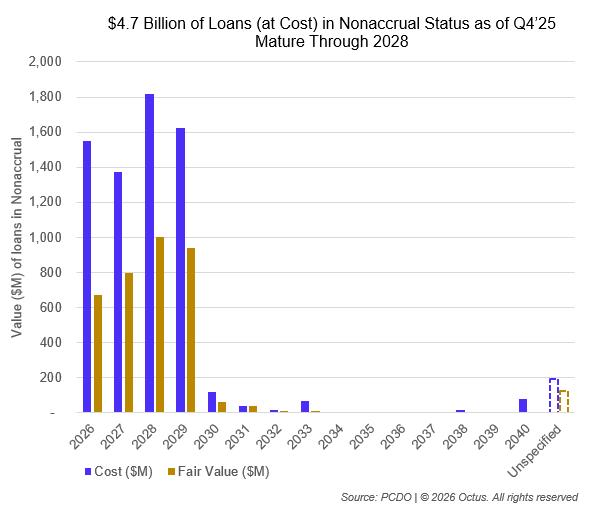

BDC Q4'25 Nonaccruals

|

|

|

|

Click above to access content

Additional Registration Required

|

|

|

|

|

In the News

|

|

overreaction or bubble?

|

|

|

|

Click above to access content

Additional Registration Required

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Bankruptcy and Restructuring Primer for the C-Suite and the Board

|

|

April 22, 2026

|

| Learn More |

|

|

|

|

|

|

Inside Credit Investors' Use of AI

|

|

April 23, 2026

|

| Learn More |

|

|

|

EMTA Forum: 2026 EM Corporate Bond Outlook in Boston

|

|

April 23, 2026

|

| Learn More |

|

|

|

ABI: Structure and Implications of Liability-Management Exercises

|

|

April 30, 2026

|

| Learn More |

|

|

|

|

|

ABI: New York City Bankruptcy Conference

|

|

May 20-21, 2026

|

| Learn More |

|

|

|

|

|

|

|

|

The Data Download

|

|

Bringing Transparency to the Bankruptcy Process

|

|

|

|

|

|

Click Above to Access The Data Download

|

|

Our Take:

The Daily Cost of BK Legal fees Are Increasing.

Are we shocked? No.

We took a deep dive to see what is driving up the daily cost of restructurings and the culprit: Increasing Legal Hourly Rates. We analyzed final fee apps for top debtor law firms from 2018 to 2024 and found average hourly legal fees have increased by over 65% since 2018. Maybe a little bit of sunlight is the right disinfectant to help remedy the problem....

|

|

|

|

|