Creditor Corner |

|

|

Your weekly curated content from the Creditor Rights Coalition |

Over 3,700 member subscribers and growing! We bring you exclusive content from leading data and research providers Sign Up Here |

Sprayregen heads to Paul Weiss in Mega Trade, Houston and New Jersey chart different courses, Scott Goodwin on private credit, Mega Broadband lenders turn the tables, the collapsing doctrine, and much, much more…

Featured Content Bruce Richards on the Markets ““Watchin’ some good friends screamin’, ‘Let me out’” – David Bowie

|

Scroll through to read all ou?r content? |

|

|

|

Tweet of the week |

|

Click Above to Access Content |

|

|

|

|

|

In the news |

I’ts good to be the king |

|

|

Click above to access content |

|

|

|

|

|

Exclusive Content |

Houston and New Jersey chart different paths |

|

|

Click above to access content |

Our Take: The classic “liquidation bluff” used by mega-debtors and senior lenders to force biased deals is losing its teeth, at least in the SDTX. Judge Lopez’s subtle yet noticeable pushback in First Brands against the Debtors Plan and rejection of the Ascend Elements DIP could signal a major fracture in Houston’s historically predictable, pro-debtor ecosystem. Meanwhile, the New Jersey courts seem to be charting a course towards more predictable debtor-friendly terrain. |

|

|

|

|

|

Featured Content |

The Quiet Restructuring Boom |

|

|

Click above to access content |

|

|

|

|

|

Featured Content |

Private Credit’s Reckoning Is Here |

|

Click above to access content |

|

|

|

|

|

Exclusive Content |

Mega Broadband lenders turn the tables |

|

|

Click above to access content One-time registration required |

Our Take: ?Cable One tried to impose a classic prisoner’s dilemma on Mega Broadband lenders by giving them less than 24 hours to participate in a coercive exchange backed by the threat of a drop-down transaction. Instead, lenders organized and flipped the script, forcing an interim stalemate. The new playbook is not as one-sided as in days past. We’ll be watching for the next shoe to drop… |

|

|

|

|

|

Exclusive Content |

The House Always Wins (But Which House?) |

|

|

Click above to access content One-time registration required |

Our Take: ?Icahn is bringing the liability management playbook to M&A –his plan strips assets into an unrestricted subsidiary using Caesars’ own covenant capacity: a $975m investment basket together with a $500m RP basket, turning tools originally designed for defensive restructurings into weapons for a hostile takeover. |

|

|

|

|

|

Featured Content |

|

““Watchin’ some good friends screamin’, ‘Let me out’” – David Bowie (Under Pressure)

Bowie’s lyrics come to mind when I think about the outsized risk some managers have taken in the software sector.

The ultimate outcome of this cycle won’t be known until it is fully tested, probably over the next three years. Valuations have compressed significantly, yet margins and operating profits have remained relatively stable. Many investment managers know pain is coming, even as many companies remain hopeful for now.

Dr. Stewart Myers, the renowned MIT Sloan professor, introduced the concept of “debt overhang” in his seminal 1977 paper, Determinants of Corporate Borrowing. Debt overhang describes how excessive leverage distorts incentives: equity holders may forgo positive-NPV investments because much of the value created accrues to creditors. The result is constrained decision-making, reduced investment in CapEx and business development, and gradual value erosion. This becomes particularly dangerous during periods of paradigm shift, when companies need every available resources to compete.

Today’s SaaS landscape amplifies this risk.

AI has arrived. Highly leveraged software companies are carrying significant levels of debt incurred at peak valuations (last five years), during the direct lending boom. To remain competitive, these businesses will need to marshal substantial resources in the years ahead, however when Debt/EBITDA soars to 6–10x range while public SaaS EBITDA and revenue multiples have now been cut in half, many managers must be screaming, “Let me out.”

Cursor, Claude Code, and Codex enable hyperscalers and startups to build software at a fraction of the historical cost and in a matter of days, often delivering comparable or enhanced functionality at significantly lower price points. Legacy seat-based SaaS models face compression, margin pressure, and ultimately the potential for obsolescence.

In distress situations, the dynamic becomes even more severe. Customers grow reluctant to remain with a troubled vendor, recurring revenue weakens, and recovery values decline.

The software cycle is only beginning to separate disciplined deployment from aggressive underwriting. Private credit managers with less than 10% software exposure have been prudent, I believe. Those with 20%+ SaaS exposure must face the realities of AI-driven disruption.

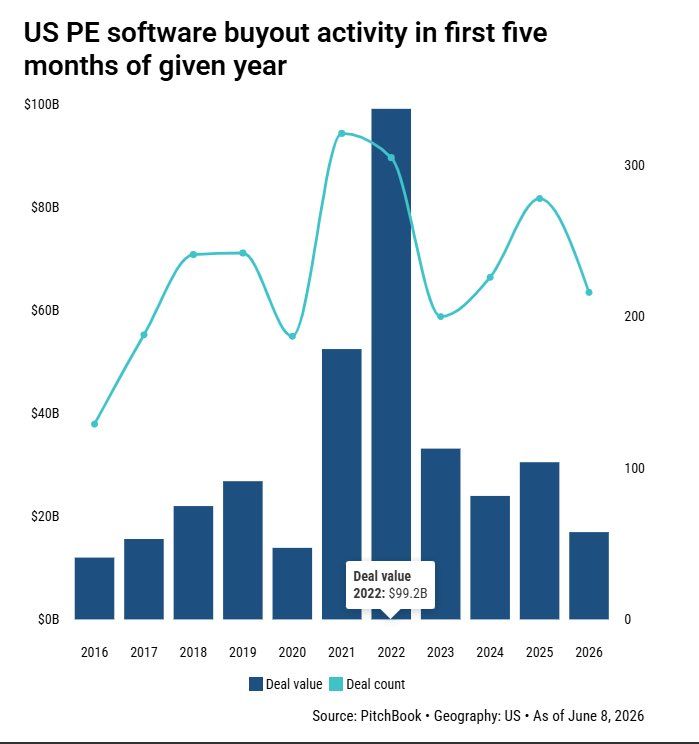

This chart below, shows continued investment flowing into software sector this calendar year, however I have to call this out, because I don’t believe the numbers, as I assume these deals were committed to by PE and lenders prior to the SaaSpocalypse, which likely means the deals were announced in Q3/Q4 of 2025 and just closed in 2026.

Recent quote from a Direct Lender: “Don’t even think about it. We have too much software exposure. We are not going to fund another software buyout.”

Bottom line: Liquidity is evaporating for highly leveraged legacy software.

|

|

Click above to access content To follow Bruce’s thoughts on the markets, investing and more, follow @bruce_markets |

|

|

|

|

|

Exclusive Content |

It’s Not Fraud If You Do It in Steps (Maybe) |

|

|

Click above to access content |

Our Take: The courts still can’t agree on whether a multistep LME is one big heist or just a series of totally unrelated coincidences.

The collapsing doctrine sounds like something out of a physics lecture, but it’s really just courts asking: “Did you chop this deal into pieces specifically so we wouldn’t notice what you were doing?” In Wesco, a Texas judge said “I see separate steps, I follow the text, good day.” In STG and Hunkemöller, New York’s Justice Patel said “nice try” and let excluded lenders proceed. Same doctrine, completely different outcomes. Until an appellate court picks a side, venue is everything – and the stakes for getting it wrong are getting higher. |

|

|

|

|

|

Webinar Replay |

Outlook on the European Special Situations Market |

|

Click above to watch |

|

|

|

|

|

|

|

|

|

|

|

TMA NYC Joint Pop Up Happy Hour |

June 30, 2026 |

| Learn More |

|

|

|

Fitch Ratings & REDD Intelligence: Panel Discussion on Latin America Sovereign and Corporate Credit |

July 15, 2026 |

| Learn More |

|

|

|

|

|

|

|

|

|

|

The Data Download |

Bringing Transparency to the Bankruptcy Process |

|

|

|

|

Click Above to Access The Data Download |

Our Take: The Daily Cost of BK Legal fees Are Increasing. Are we shocked? No. We took a deep dive to see what is driving up the daily cost of restructurings and the culprit: Increasing Legal Hourly Rates. We analyzed final fee apps for top debtor law firms from 2018 to 2024 and found average hourly legal fees have increased by over 65% since 2018. Maybe a little bit of sunlight is the right disinfectant to help remedy the problem…. |

|

|

|

|

|

|