The Elephant in the Room President-elect Trump’s economic agenda + Fed easing cycle = Risk-On

The Fed cut rates 25bps as expected to a target range of 4.50% to 4.75%. Chairman Powell is on course to lower rates 25bps in December; however, I interpret Powell’s remarks to be slightly hawkish as he will be vigilant before eventually arriving at the neutral rate. Fed policy may conflict with the new administration’s desire for lower rates to reduce government funding costs. Powell emphasized that the election outcome will not impact “near term” policy decisions, and furthermore Powell mention that fiscal and trade policy may create greater growth and potentially/higher inflation requiring a higher terminal rate than what the market is assumes. Fed Funds futures lands at 3.7% in Q1 of 2026, one quarter prior to the end of Powell’s term expiring.

The Elephant in the Room was when Powell was asked whether he would resign if President-elect Trump asked him to resign and Powell answered in one word: “No.” The follow-on question related to whether the President has the legal rights to fire or demote him when Powell said: “Not permitted under the law.” The President can only fire a Fed Chairman “for cause.”

A little drama makes for an interesting news cycle, but there is no drama for the markets – it’s Risk-On!

Five Take-a-ways to digest as we enter the weekend and reflect on this meaningful & memorable week: ? 1. Stronger USD: 1) higher interest rate differentials v. G7 countries, 2) US remains the strongest growth economy in the developed markets, 3) capital flows to the US to increase

2. Vibrant equity market: 1) Trump 2.0 = lower corporate tax rate, 2) earnings growth above trend as 2025 (E) +14% EPS for S&P 500, 3) regulatory relief is hugely positive

3. Corporate credit spreads to tighten & remain tight: 1) credit profiles and debt-to-EBITDA ratios improve, 2) lower default rate probabilities, 3) credit ratings improve

4. PE Activity will surge: 1) LBO volumes increase with lower SOFR rates, 2) PE begins to harvest gains allowing for improved DPI, 3) Dividend Recaps surge

5. Private Credit will deliver: 1) origination volume to increase commensurate with PE activity, 2) loss rates fall improving loss-adjusted returns, 3) significant IRR differential v. cash/UST/Corp Spreads

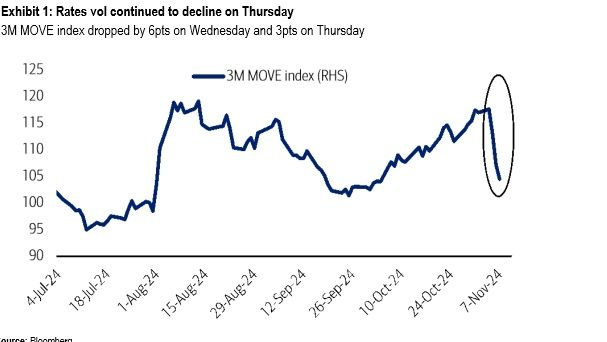

Interest Rate volatility will begin to settle down, rates will level off as the US economy is on solid ground. |