?The Fed’s Mixed Signals: Strategy or Confusion?

Yesterday’s Fed meeting was crystal clear: hold rates steady for now. What’s less clear is the confusion they seem to have with respect to basic monetary policy. Let me explain this and provide a few insights.

– The Fed cut rates 100bp from September since December ‘24, but during this same period when they were “easing,” the Fed was ‘tightening” by conducting Quantitative Tightening (QT) – running off/selling $60 billion per month of US treasuries ($25B) plus 30-year mortgages ($35B). It NEVER makes sense to ease while tightening since these two policies by the same entity run counter. In years prior, during Chair Powell’s earlier tenure, the Fed previously did the exact opposite, which also made no sense – they were conducting QE (bring down UST rates) while they were raising their lending rate.

– Reducing QT from $25B UST per month to $5B per month has effectively ended QT for now. This move will take pressure off the treasury market, which is a good idea since ‘25/26 will be record years for treasury issuance.

– On the other hand, the Fed will keep selling 30-year mortgages, liquidating $35B from their mortgage holdings per month. While the Fed has lost a fortune having purchased these mortgages at all time low rates, the Fed is now selling these mortgages, which serves to keep mortgage rates higher than otherwise, delaying delaying decisions to buy for many potential homeowners.

– If the Fed had not conducted financial repression for so long during the crazy ZIRP days, they wouldn’t be in the position they find themselves in today.

– Since the Fed eased 100bps a few months ago, GDP has slowed/inflation has picked up, not the economic response they had hoped for.

– Powell said: “uncertainty around the economic outlook has increased,” which most Fed watchers view as “dovish.”

– Yesterday, the Fed increased its inflation expectation, core PCE from +2.5% to +2.8%, while they reduced GDP growth expectations from +2.1% to +1.7% for 2025. Powell removed language suggesting that risks to inflation and employment are balanced, since cracks have clearly appeared.

– No stagflation risk yet, but we have clearly moved two steps in that direction.

– More zero dots were announced; the average remains 2 cuts expected in 2025 (market says 3).

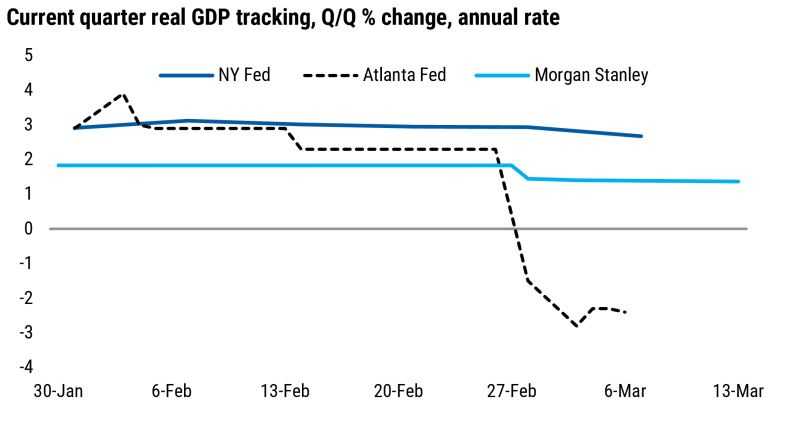

– Most perplexing for me to comprehend is how the NY Fed is estimating GDP to grow at 1.7%, while the Atlanta Fed is expecting GDP to fall by 2.5% in Q1 of 2025 as seen in below chart.

The Fed Chair job is difficult, navigating a complex marketplace, evaluating the strength of the banking system, managing inflation and employment, which is their dual mandate, forecasting the impact from uncertain fiscal policy that is beyond their control or often counter to what they are trying to accomplish, potential impact from tariffs, and facing intense public scrutiny from Fed watchers and pundits like me. Bonds fairly priced, Credit investors rejoice.

|