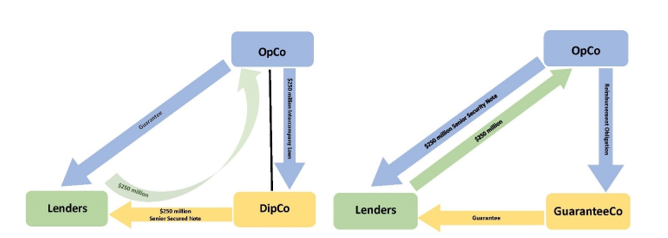

As we see, the situations are similar. First, in both instances, the lender lends the money to OpCo, the ultimate recipient. In the double dip situation, the money supposedly passes through DipCo, but only for an instant. (And again, in practice, the money might flow directly from the lenders to OpCo.)

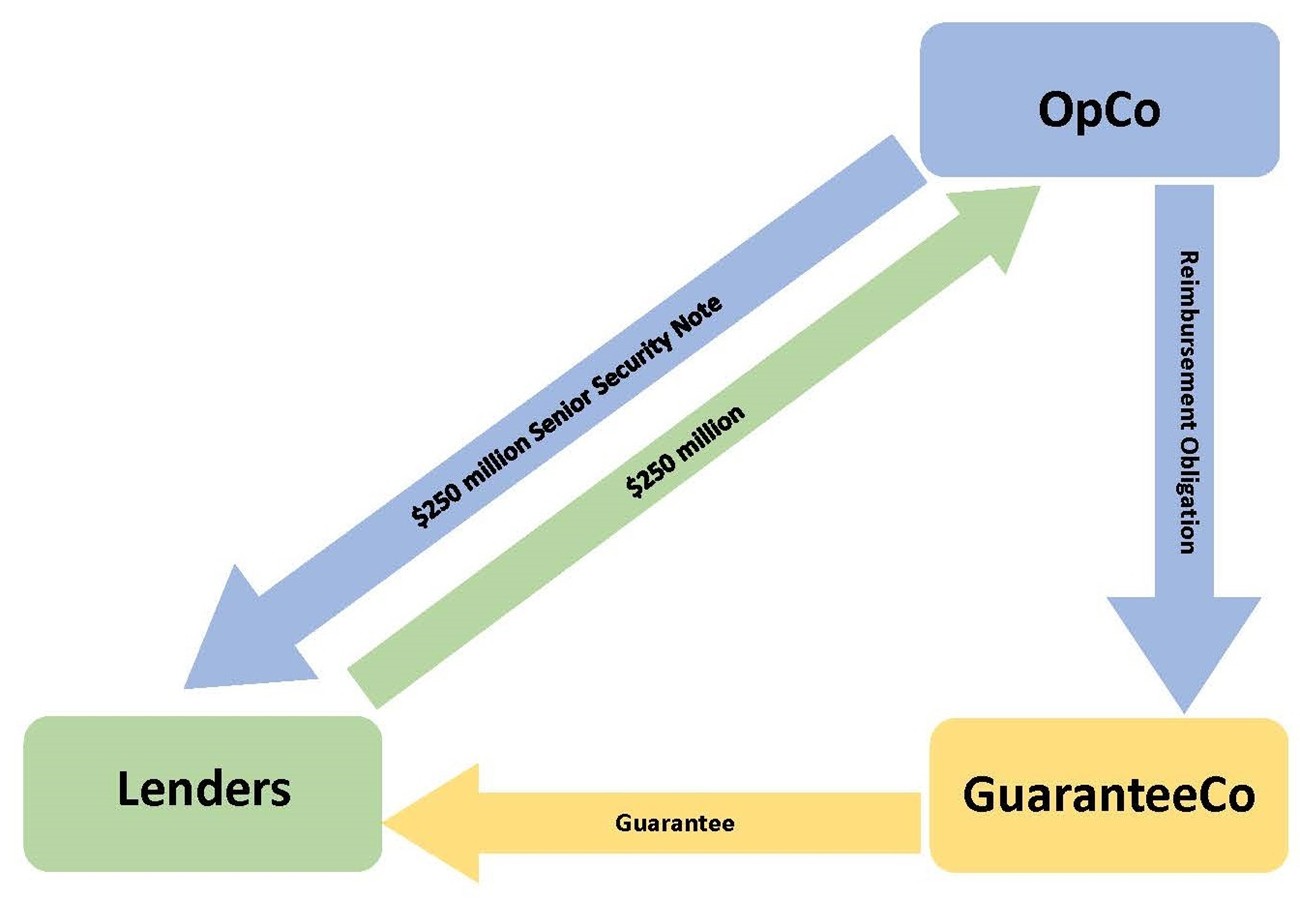

Second, the lenders have two claims, one against OpCo and one against the other entity (either GuaranteeCo or DipCo, as the case may be). The claim against OpCo is denominated a “guarantee” in the double dip situation, but call it whatever you want, it is a direct claim against OpCo for payment of the debt to the lenders.

Third, the other entity (GuaranteeCo or DipCo) has a claim against OpCo, for which it would use the funds to repay the lenders. In the guarantee situation, the claim is a reimbursement claim (which may or may not be the subject of a separate agreement). In the double dip situation, the claim is a claim on a receivable for money purportedly lent to OpCo.

Of critical importance, the substance looks very similar: the lenders have made a loan ultimately to OpCo for which they may look to OpCo and the other entity for repayment. The documents just call it something different. Should that be enough to take it outside the scope of Section 502(e)(1)(B)?

We’ve all heard about courts looking through the form to the substance of a transaction. Courts also look to the economic reality of a situation as opposed to “dictionary definitions and formalistic labels.” A willingness of a court to look past labels—to the substance as opposed to the form—would be critical in determining whether to disallow the double dip as violative of Section 502(e)(1)(B).

Here, a court might look at this situation in substance to be a loan to OpCo guaranteed by DipCo. While the documents are labeled as something other than a loan to OpCo guaranteed by DipCo, the substance shows that the situations are entirely similar. Moreover, it may well be that the situation was engineered to allow for a double dip, expressly contrary to the equitable considerations of the Bankruptcy Code. …. Conclusion Section 502(e)(1)(B) of the Bankruptcy Code seeks to disallow multiple claims that seek to repay a single debt—the so-called “double dip.” It is meant to codify the equitable notion of fairness among creditors and equality of distribution. By its statutory terms, however, it is limited to contingent claims for reimbursement or contribution.

While a Court has never ruled on the applicability of Section 502(e)(1)(B) to a double-dip financing to the author’s knowledge, Section 502(e)(1)(B) may well have application to the financing double dip world.[7] If a court were to look through the form to the substance and economic reality of a given situation, it could use this section to prevent the double dip. Moreover, by its very terms, Section 502(e)(1)(B) may apply.

The foregoing analysis focuses on the simple double dip structure. In practice, a double dip may be much more complex, with additional entities and correspondent claims entering the mix. That said, one always has to be on the lookout for a claimant seeking a double-dip recovery. In that circumstance, Section 502(e)(1)(B) may present a statutory obstacle to double dips. |