Less Violence More Cooperation

Creditor on Creditor Violence occurs when one group of creditors take a position adverse to remaining creditors within the same class to take advantage of the flexibility in the loan agreement to capitalize at the expense of other creditors. Until now, this hostile move to structurally subordinate other creditors (including CLO holders) has been too commonplace for a company with excess debt. Creditors recently took a different approach, which achieves a favorable outcome by working together through a Cooperation Agreement (“Co-op”). Big Shout-out to Gibson Dunn, the law firm that has established the framework/procedural measures allowing all creditors to work consensually vs. the overly aggressive technique known as creditor-on-creditor violence.

Yesterday, Altice France (2nd largest telecom) creditors announced a comprehensive liability management transaction using a Co-op agreement that includes creditors holding both senior and junior debt. The creditors banned together and negotiated with Altice France with one common voice in response to Altice’s (France) March ‘24 announcement to deleverage from 6.4x debt/EBITDA to less than 4.0x debt/EBITDA, with an intention to capture ~€10bn of discount from its creditors. Creditors didn’t take kindly to Altice’s (France) intention to move its valuable fiber, mobile and data center assets out of the reach of creditors. When the news hit, the senior debt fell 20 points while the junior debt fell 50 points.

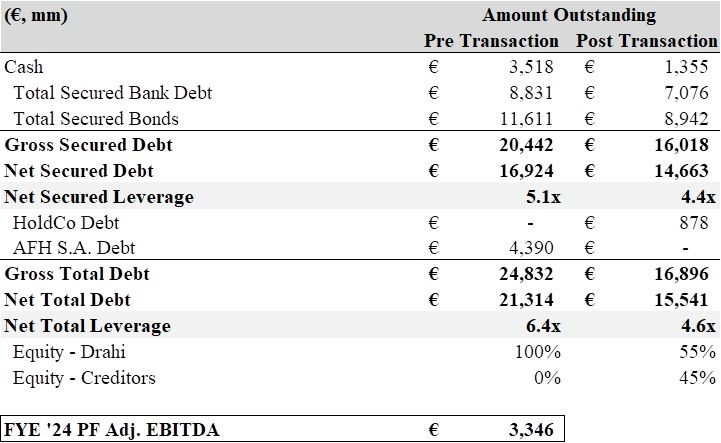

Creditors organized & retained the brilliant legal minds from Gibson Dunn who worked judicially to establish the Co-op, a plan whereby all creditors could work together so that the Company would not be capable of dividing the group that might typically end in creditor-on-creditor violence. After months of intense negotiation, a consensual deal was reached. Senior creditors swapped their debt for 77c of new debt +10c of cash + 31% equity in Altice France. Junior creditors swapped their deeply discounted debt for 20c of new debt + 5c of cash + 14% of equity in Altice France. All debt maturities were extended 3-years providing significant runway. Patrick Drahi, the controlling shareholder, maintained 55% of the equity. Mr. Drahi funded the cash payments to creditors from the assets previously clawed away from creditors. This allowed the Company to deleverage to 4.6x and enabled Mr. Drahi and creditors to become aligned to maximize the value of the company.

Thus far, the senior package traded back to roughly 90c with further upside while the junior debt is also poised for strong upside through its new debt and equity. See new capital structure below.

Next big Co-op is right around the corner, a U.S. healthcare company where Marathon is also working with creditors and the Company.

Motto of the Day: Less violence, more cooperation is the way to go |