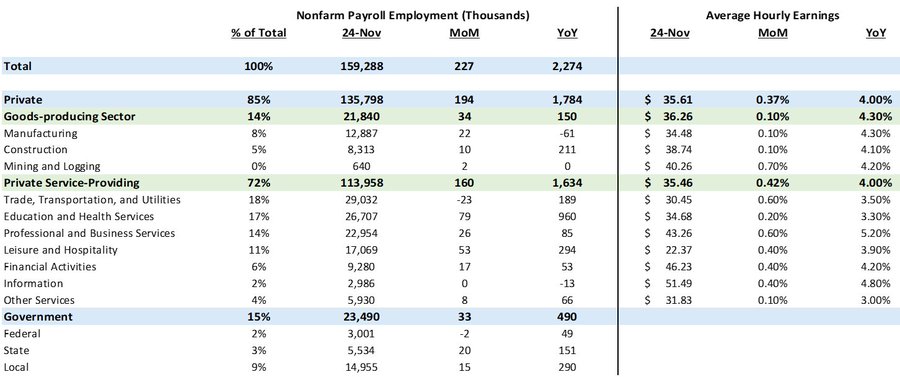

Employment Jumps

Employment jumps +227k in November (+220k forecast) with wage gains strong, +0.37% MoM and 4.0% YoY, however, the unemployment rate moved up from 4.1% to 4.2%.

Jobs gains led by Education and Health Services, Leisure and Hospitality, Manufacturing, and Business Services. Interesting, the only two categories to lose jobs were Trade, Transportation and Utilities & Federal Government.

Looking forward, we should expect more government jobs cuts to come with DOGE swinging into full swing, with likely gains from Manufacturing given tariff policy.

Expect the Fed to lower rates 25bps (90% probability) on December 18, tallying 100 bps lower since September 18 (3 months). Fed cuts are positive for markets, however, with strong U.S. economic data (2.5% GDP gains & 3% inflation), it’s pace will slow since there are 8 FOMC meetings next year (and only 3 cuts expected for 2025). Regardless of whether you think the Fed should ease or pause, my outlook is super positive for credit markets.

I expect spreads to remain tight across the credit spectrum in 2025 as macro backdrop is hugely supportive. High Yield and Broadly Syndicated Loans yield just inside of 7%, which is close to historical norms, while Private Credit is forecasted to generate 11-12% IRR. Risk-on & U.S. exceptionalism remains the winner in this environment. The best risk-reward within the alternative credit markets is private credit (Middle Market Loans & Asset-Based Loans are my 2 favorite segments).

|