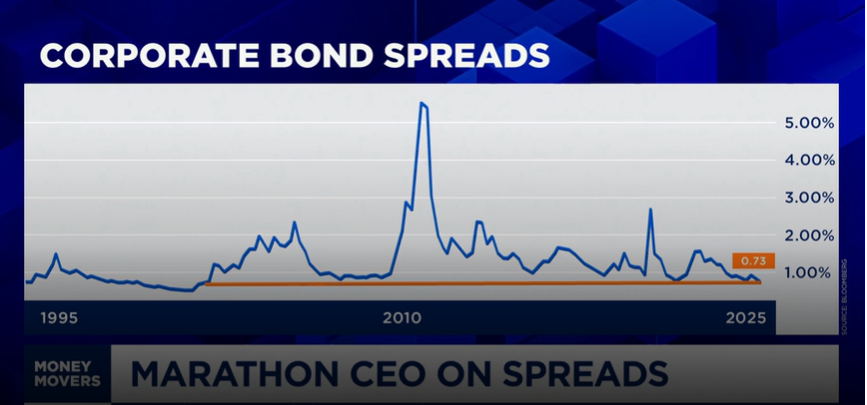

Tight as a Drum (+76 bps)

Investment Grade Corporate Credit Spreads trade at the 0 percentile, a spread of +76 bps vs. UST, the tightest spread since 1997 (see table above). A-rated bonds trade at +62 bps, while BBBs are +96bps.

Reasons why spreads are so tight: – Credit risk and balance sheets has improved for IG issuers – Credit conditions in the financial markets are at its easiest level since pre-COVID – The Fed will soon embark upon an easing cycle – Corporate earnings are strengthening – The risk of recession is low – Investor Demand is robust (higher UST yields allows the absolute yield level to remain ~50%, despite tight spreads)

These strong fundamentals paint a supportive picture for IG credit; however, historically tight spreads suggest that much of the positive outlook is already reflected in current pricing. Investors should remain disciplined and selective, with no reason to sell IG at the current juncture as our favorable credit conditions should remain intact. Since diversification and intelligent asset allocation decisions remains paramount to long-term wealth creation, capital allocators can identify compelling non-IG and Private Credit that will continue to offer higher IRR/MOIC profiles as yield premiums for higher yielding assets should continue to meaningfully enhance portfolio income, just as it has over the years. |