|

““Watchin’ some good friends screamin’, ‘Let me out’” – David Bowie (Under Pressure)

Bowie’s lyrics come to mind when I think about the outsized risk some managers have taken in the software sector.

The ultimate outcome of this cycle won’t be known until it is fully tested, probably over the next three years. Valuations have compressed significantly, yet margins and operating profits have remained relatively stable. Many investment managers know pain is coming, even as many companies remain hopeful for now.

Dr. Stewart Myers, the renowned MIT Sloan professor, introduced the concept of “debt overhang” in his seminal 1977 paper, Determinants of Corporate Borrowing. Debt overhang describes how excessive leverage distorts incentives: equity holders may forgo positive-NPV investments because much of the value created accrues to creditors. The result is constrained decision-making, reduced investment in CapEx and business development, and gradual value erosion. This becomes particularly dangerous during periods of paradigm shift, when companies need every available resources to compete.

Today’s SaaS landscape amplifies this risk.

AI has arrived. Highly leveraged software companies are carrying significant levels of debt incurred at peak valuations (last five years), during the direct lending boom. To remain competitive, these businesses will need to marshal substantial resources in the years ahead, however when Debt/EBITDA soars to 6–10x range while public SaaS EBITDA and revenue multiples have now been cut in half, many managers must be screaming, “Let me out.”

Cursor, Claude Code, and Codex enable hyperscalers and startups to build software at a fraction of the historical cost and in a matter of days, often delivering comparable or enhanced functionality at significantly lower price points. Legacy seat-based SaaS models face compression, margin pressure, and ultimately the potential for obsolescence.

In distress situations, the dynamic becomes even more severe. Customers grow reluctant to remain with a troubled vendor, recurring revenue weakens, and recovery values decline.

The software cycle is only beginning to separate disciplined deployment from aggressive underwriting. Private credit managers with less than 10% software exposure have been prudent, I believe. Those with 20%+ SaaS exposure must face the realities of AI-driven disruption.

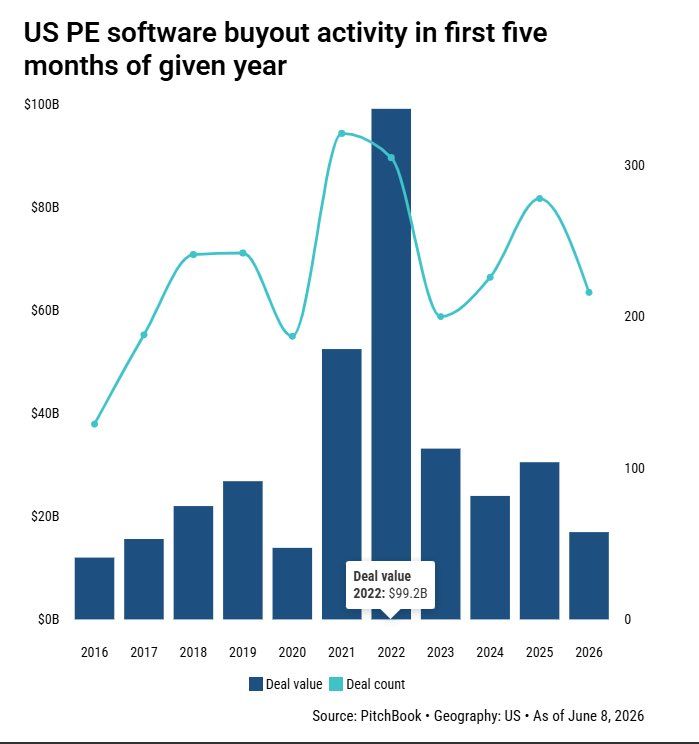

This chart below, shows continued investment flowing into software sector this calendar year, however I have to call this out, because I don't believe the numbers, as I assume these deals were committed to by PE and lenders prior to the SaaSpocalypse, which likely means the deals were announced in Q3/Q4 of 2025 and just closed in 2026.

Recent quote from a Direct Lender: "Don't even think about it. We have too much software exposure. We are not going to fund another software buyout."

Bottom line: Liquidity is evaporating for highly leveraged legacy software.

|