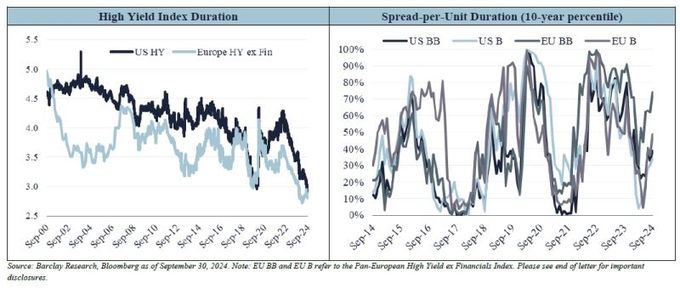

High Yield: Strong Credit Quality, Low Duration

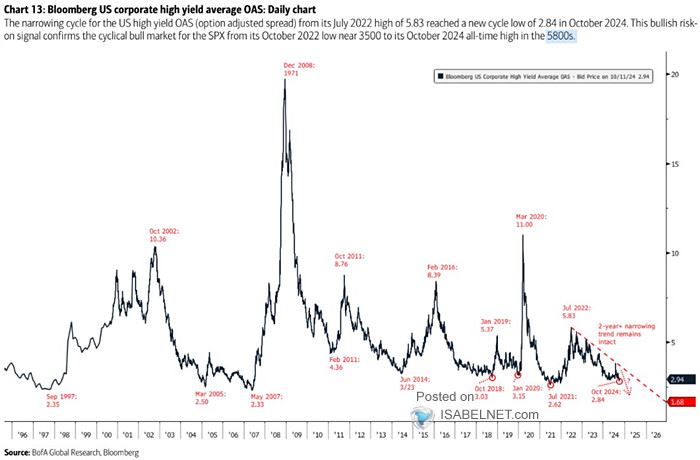

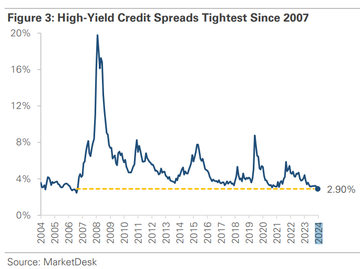

The High Yield (HY) Bond sector is stronger than ever, characterized by robust BB-rated bonds and improving credit profile of single B-rated bonds. HY bond spreads are tighter than its historical average for two key reasons that 100% justify tighter spreads: – HY bond duration for US and Europe is at an all-time low, with effective durations under 3 years, for the first time ever as can be seen in the chart below. Shorter duration strong credit trades at tighter spreads than the same names with longer-term maturities. Fundamental improvement in lower-quality borrowers whose debt trades yield-to-call plus higher quality borrowers delaying refinancing existing debt, waiting for better market conditions are the technical reasons. Spreads on BB and B-rated credits are within historical ranges when adjusted for duration.

– HY bond defaults remain relatively low while recoveries are above long-term averages, reducing the overall impact of defaults on high-yield portfolios. A large cohort of HY borrowers will likely issue bonds in the coming quarters, with the net impact that the average coupon for US HY market will adjust higher. The average coupon has already risen from ~5.7% in 2022 to ~6.5% today, with more to come. HY managers are well-positioned to benefit from higher interest income with credit fundamentals improving further. As long as the economy remains vibrant and earnings growth continues, tight HY spreads will prevail. HY bonds are an important component for Multi-Asset Credit (“MAC”); one of the four sectors along with Broadly Syndicate Loans, EM Bonds, and Structured Credit. Institutional Investors or large Capital Allocators recognize the merits of MAC as managers are able to navigate across the 4 major sectors of global credit to uncover value. |