Creditor Corner |

|

|

Your weekly curated content from the Creditor Rights Coalition |

Over 3,700 member subscribers and growing! We bring you exclusive content from leading data and research providers Sign Up Here |

?In this Week’s Creditor Corner Del Monte’s Confirmation and implications for Serta, Judge Kaplan speaks up!, First Brands in a frenzy, CasteKnight blocking Trinseo’s dunk, Jeld-Wen, and much, much more…

Featured Content Bruce Richards on the Markets |

Scroll through to read all ou?r content? |

|

|

|

Exclusive Content |

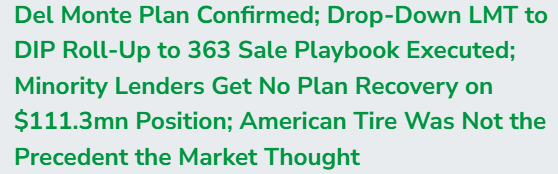

A Momentous Confirmation! |

|

|

Our Take: A great analysis of the the distressed playbook from pre-petition LME as de facto Chp11, to minority lender holdout success post Serta decision, to landing in Judge Kaplan’s court to experience the latest trends in mediation and challenges to non pro-rata roll-ups.

Judge Kaplan’s decision on non pro-rata roll ups stands in contrast to Judge Goldblatt’s decision and creates a cash versus cashless distinction that could turn the entire LME playbook upside down (see Serta below).

The broader lesson is that out-of-court litigation seemingly now requires as much luck as legal merit. For minority lenders today, the choice is increasingly stark: join the ad hoc group or risk being marginalized when the restructuring inevitably moves into court. |

Click above to access content One-time registration required |

|

|

|

|

|

Exclusive Content |

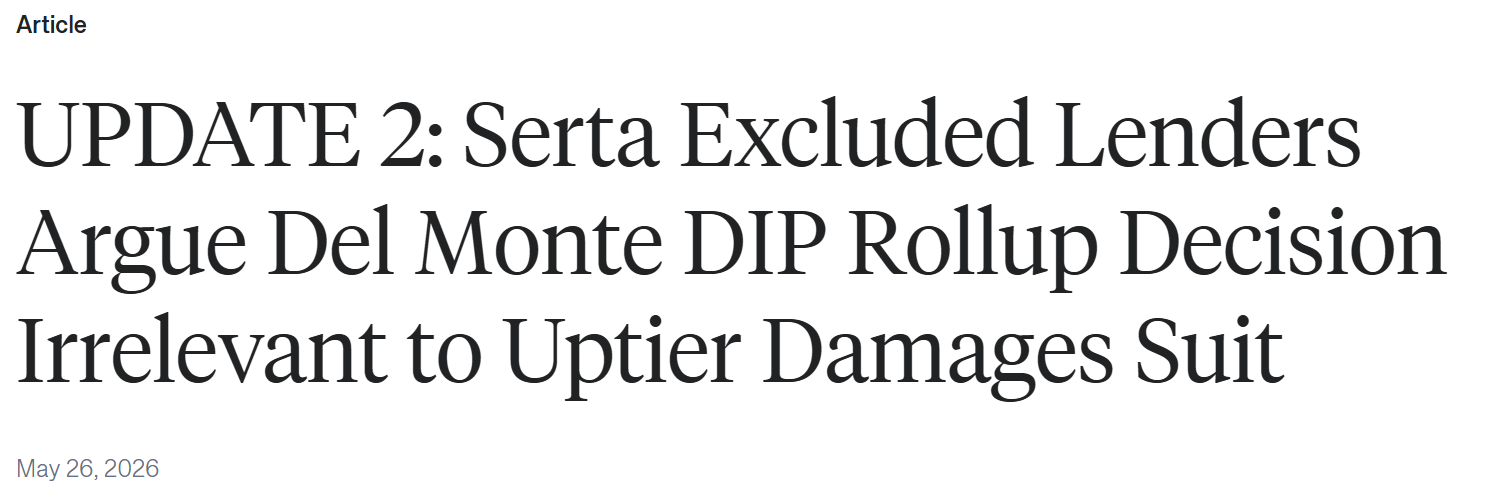

Serta meets Del Monte…. |

|

|

Click above to access content |

Our Take: Judge Kaplan’s Del Monte decision is already reverberating through the Serta litigation, where participating uptier lenders are arguing that pro rata sharing provisions apply only to actual cash payments—not to a cashless exchange of existing debt for new debt.

Say What?? ? If taken to its logical conclusion, the argument suggests that the “cashless” exchange feature embedded in virtually every modern liability management transaction—including many uptiers and roll-ups—does not even implicate the pro rata sharing provisions.

That certainly appears to be one implication of Judge Kaplan’s reasoning. But it is also why we expect the ultimate reach of the decision to be more limited than some market participants currently suggest.

Still, the decision raises a provocative question: if exchanging old debt for new super-priority debt is not a “payment,” when exactly is value being transferred for purposes of a pro rata covenant?

That debate is now front and center in Serta and other liability management disputes. While Del Monte may ultimately prove to be a fact-specific ruling, its ripple effects are likely to continue as lenders test the boundaries between cash payments, cashless exchanges, roll-ups, and other forms of non-pro rata treatment. |

|

|

|

|

|

Podcast of the Week: |

How to navigate sector-specific distress… |

|

Click above to access content |

|

|

|

|

|

Exclusive Content |

Double-Dip Decision coming soon…? |

|

|

Click above to access content One-time registration required |

Our Take: ? Trinseo filed chapter 11 this week labeling its case as “pre-packaged” — the latest buzzword in the restructuring toolkit. As our friends Max Frumes and Cat Corey of 9fin rightly point out, Trinseo appears much closer to a pre-arranged deal dressed up in prepack clothing.

?The excluded lenders’ 40% confirmation-blocking position gives them meaningful leverage in a key voting class, creating a dynamic where litigation outcomes and plan negotiations are deeply intertwined. Judge Lopez may ultimately have to define the limits of basket capacity, but the path to emergence could be determined by who blinks first. |

|

|

|

|

|

Exclusive Content |

2017 IPO turned 2016 LME |

|

Click above to access content One-time registration required |

|

|

|

|

|

Exclusive Content |

First Brands in a frenzy! |

|

|

|

Click above to access content One-time registration required |

|

|

|

|

|

Exclusive Content |

throwing hands in the Wild West |

|

|

|

Click above to access content |

Our Take: ? Another “pre-packaged” case with trappings of a much more traditional restructuring with preferred holders’ motion to terminate exclusivity and the debtors’ confirmation motion coming before Judge Perez on the same day next week. In an era dominated by prepackaged bankruptcies, the preferred holders are making a rare attempt to push back against a process that increasingly leaves little room for negotiation once a case is filed.

If successful, the ruling could inject a more traditional Chapter 11 dynamic into Fifth Circuit restructurings – more negotiation, competing PoRs, and a longer stay in court. Debtors, however, are unlikely to absorb those costs willingly. Faced with greater uncertainty and expense, they may simply migrate to jurisdictions that remain more accommodating to prearranged outcomes. The fight is about more than exclusivity; it is a test of whether Chapter 11 remains a venue for negotiation or merely a mechanism for implementation. |

|

|

|

|

|

Featured Content |

|

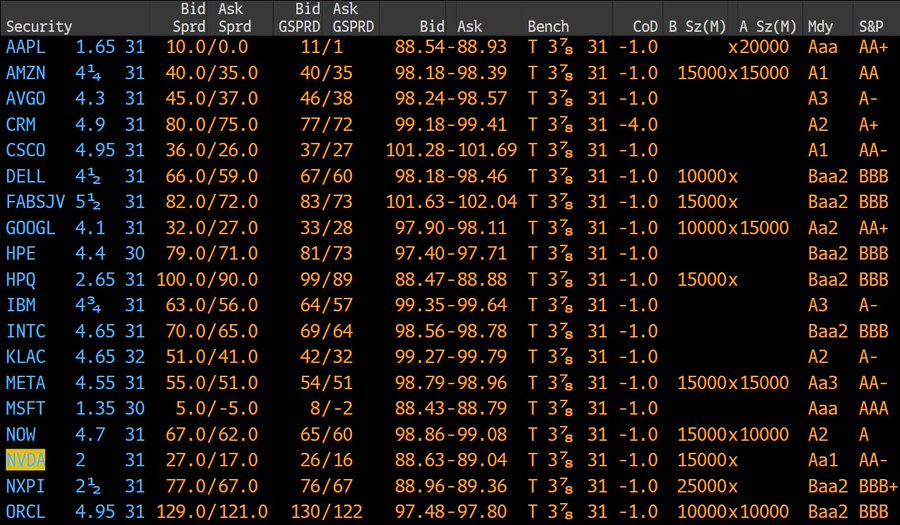

This Rising Star is the GOAT

Rising Star: the reference to a credit that migrates from High Yield to Investment Grade. The biggest leap is SpaceX, securing a $20 billion loan from Goldman Sachs, BofA, Citi, JPMorgan, and Morgan Stanley at a spread of roughly SOFR +100 bp (a mid-4% coupon) not too dissimilar to the borrowing costs of IG-rated companies such as Meta, Dell and Google (see table below for comparison vs. other IG tech companies). This is remarkable since this $20 billion loan refinances $17.5B of debt of which some yields 12%+, as the debt stack of the company held a range of +500 to 800 bps over SOFR. This saves SpaceX ~$1 billion debt service costs annually. BBB- rating, however, the rating agencies are notoriously conservative and would likely make a mistake rating SpaceX debt BB+.

Perspective 1: Currently SpaceX is non-rated currently, however, is priced as B- credit or CCC+. Looking forward, SpaceX should be able to secure a BBB- rating, however, if the rating agencies take a conservative approach, they may rate SpaceX debt BB+.

Perspective 2: Major bank lenders/investment banks have committed to underwrite next month’s IPO of SpaceX IPO and based upon the expected market value of ~$2 trillion, $20 billion in debt is relatively inconsequential as it represents a mere ~1% of market cap. Further, SpaceX will have ~$80 billion in cash post-IPO on its balance sheet, so net-debt becomes negative. Just last year (June 2025), xAI 12.5% secured notes were priced at a slight discount to par, one of the five debt facilities that is being refinanced with the new bank facility.

GOAT: The largest U.S. IPO was Facebook in 2012 at a $104 billion valuation. SpaceX is the GOAT with a valuation that is likely to be priced at ~$2 trillion. A unicorn is a venture funded startup that is privately held with greater than $1 billion valuation, and when the term was first assigned on this basis it was a rare occurrence, thus the name. There have been over 2,000 unicorns created, but SpaceX is the first $1 trillion-plus company, which is indeed a generational event for both credit and equity markets. The June 12 listing on Nasdaq (SPCX) will be a momentous day, and there will be much more for us to discuss.

|

|

Click above to access content To follow Bruce’s thoughts on the markets, investing and more, follow @bruce_markets |

|

|

|

|

|

Exclusive Content |

PC opportunities in H2 |

|

|

Click above to access content One-time registration required |

|

|

|

|

|

|

Bloomberg Global Credit Forum |

June 3, 2026 |

| Learn More |

|

|

Debtwire: Private Credit Forum |

June 3, 2026 |

| Learn More |

|

|

|

U.S. Special Situations Outlook |

June 11, 2026 |

| Learn More |

|

|

|

|

|

|

|

|

|

Featured Event |

$100 off for CRC Subscribers! |

|

|

|

| Learn More |

Click above to access content |

CRC Subscribers Receive An Additional $100 off by emailing info@creditorcoalition.org |

|

|

|

|

The Data Download |

Bringing Transparency to the Bankruptcy Process |

|

|

|

|

Click Above to Access The Data Download |

Our Take: The Daily Cost of BK Legal fees Are Increasing. Are we shocked? No. We took a deep dive to see what is driving up the daily cost of restructurings and the culprit: Increasing Legal Hourly Rates. We analyzed final fee apps for top debtor law firms from 2018 to 2024 and found average hourly legal fees have increased by over 65% since 2018. Maybe a little bit of sunlight is the right disinfectant to help remedy the problem…. |

|

|

|

|

|

|