Creditor Corner |

|

|

Your weekly curated content from the Creditor Rights Coalition |

Over 3,700 member subscribers and growing! We bring you exclusive content from leading data and research providers Sign Up Here |

?In this Week’s Creditor Corner Drahi playing hardball (again), Trinseo Challenge to double dips, Investors weigh in, Brightline off the rails, BDC Benchmarking, Michael Gatto Speaks Up, and much, much more…

Advocacy in Action CRC urges rejection of NYS legislation on Sovereign Debt Restructuring

Featured Content Bruce Richards on the Markets Michael Gatto Speaks Up |

Scroll through to read all ou?r content? |

|

|

|

|

|

Enrollment Closes Monday |

Last Chance to Enroll $100 off for CRC Subscribers! ?Join Colleagues from Oaktree, Fidelity, Goldentree, McDermott/Schulte, Brown Rudnick among other institutions |

|

|

|

CRC Subscribers Receive An Additional $100 off by emailing info@creditorcoalition.org |

| Learn More |

Click above to access content |

|

|

Tweet of the week |

|

Click Above to Access Content |

|

|

|

|

|

Exclusive Content |

This Is the Best You’ll Get |

|

Click above to access content One-time registration required |

Our take: It’s Altice and Drahi, so perhaps we shouldn’t be surprised. There was a time when companies engaging in asset transfers and other restructuring maneuvers at least tried to dress them up as efforts to “optimize the capital structure,” “preserve enterprise value,” or “fund future growth initiatives.” The euphemisms mattered because transfers made with the intent to hinder, delay, or defraud creditors can be avoided and recovered for the benefit of creditors. But now we’re apparently dispensing with the euphemisms altogether. When the stated purpose of an asset transfer is to position assets “for anticipated discussions with an investor group holding funded debt obligations,” what exactly are creditors supposed to infer? At some point, the line between aggressive liability management and evidence of intent starts to blur. |

|

|

|

|

|

Exclusive Content |

A Double Dip Too Far? |

|

|

Click above to access content |

Our Take: Trinseo’s restructuring is quickly becoming a masterclass in how far modern liability management transactions can go off the rails. Trinseo first utilized a double-dip structure, couple with a drop-down, to enhance recoveries of the preferred lenders. When that transaction failed to plug the hole, Trinseo layered on an additional LME, before ultimately filing a “pre-packaged” chapter 11 case premised on the validity of the underlying transactions. We hope to finally see a Bankruptcy Court address these highly controversial transactions. You can can read the excluded lenders opening brief here and our Contributors past commentary here. The transactions rely on “equity” contributions to the builder basket to increase capacity for the drop-down, a feature that could draw scrutiny from Judge Lopez, who is well known for focusing closely on the precise language of the governing documents, regardless of the practical consequences. If that issue ultimately proves fatal to Trinseo’s restructuring strategy, observers may fairly question the decision to seek refuge in the Southern District of Texas in the first place. |

|

|

|

|

|

Podcast of the Week: |

A must-see! |

|

|

Click above to access content |

|

|

Our take: Investors are increasingly signaling that liability management transactions have simply gone too far. At some point, the question becomes: why continue engineering ever more aggressive LMEs when a bankruptcy filing may provide a cleaner, more durable solution?

That could be music to Kirkland’s ears while sounding alarm bells for Simpson’s AI-hyperscale type investment in Nemecek, et. al…. time will tell. |

|

|

|

|

|

Exclusive Content |

DIP, Rescue, or Derailment? |

|

|

Click above to access content One-time registration required |

|

|

|

|

|

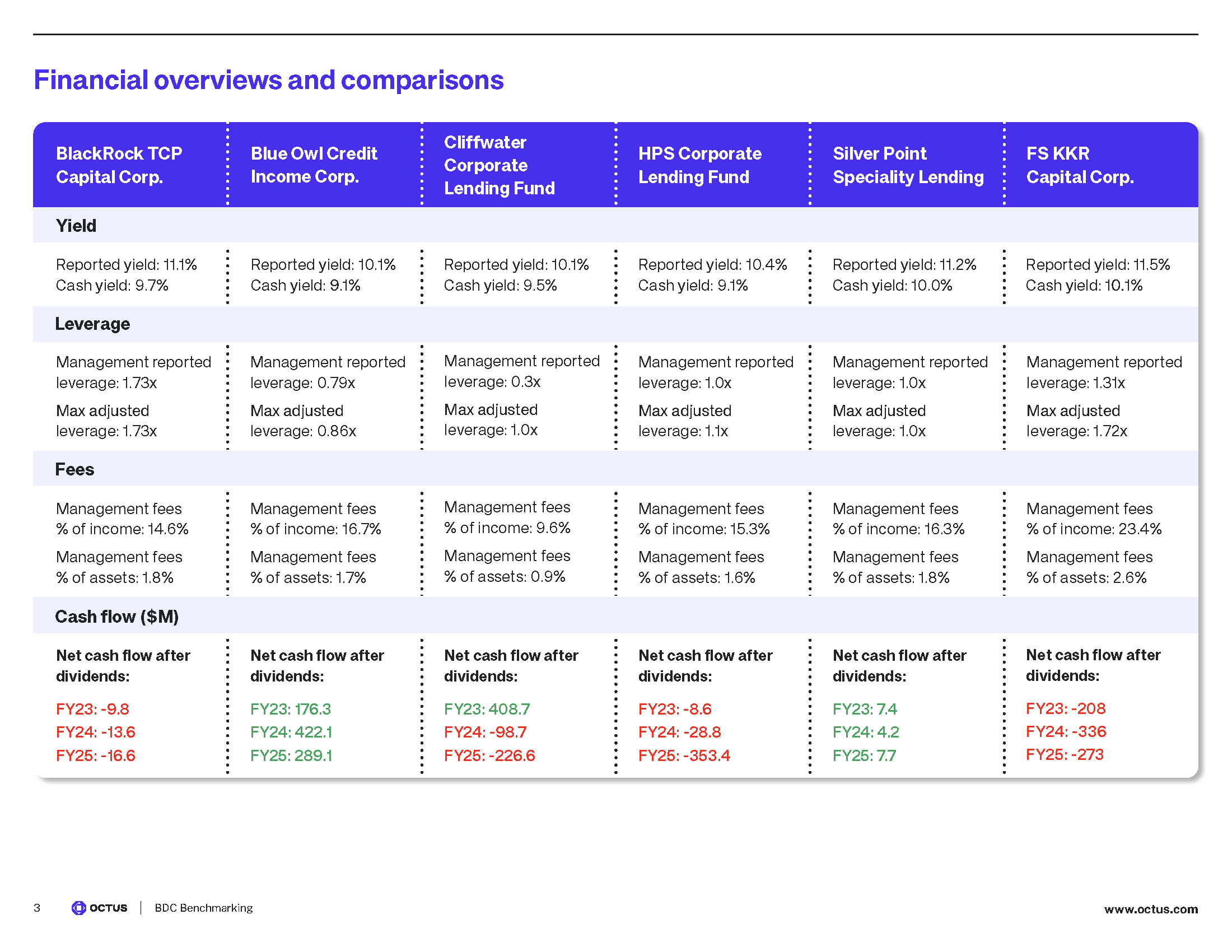

Exclusive Content |

BDC Benchmarking Briefs |

|

|

Click above to access content One-Time Registration required |

|

|

|

|

|

Featured Content |

Gatto Speaks Up |

|

|

Click above to watch |

| Watch here |

|

|

|

|

|

Exclusive Content |

UK Gains Traction as Chpt. 11 Alternative |

|

|

Click above to access content One-time registration required |

|

|

|

|

|

Featured Content |

|

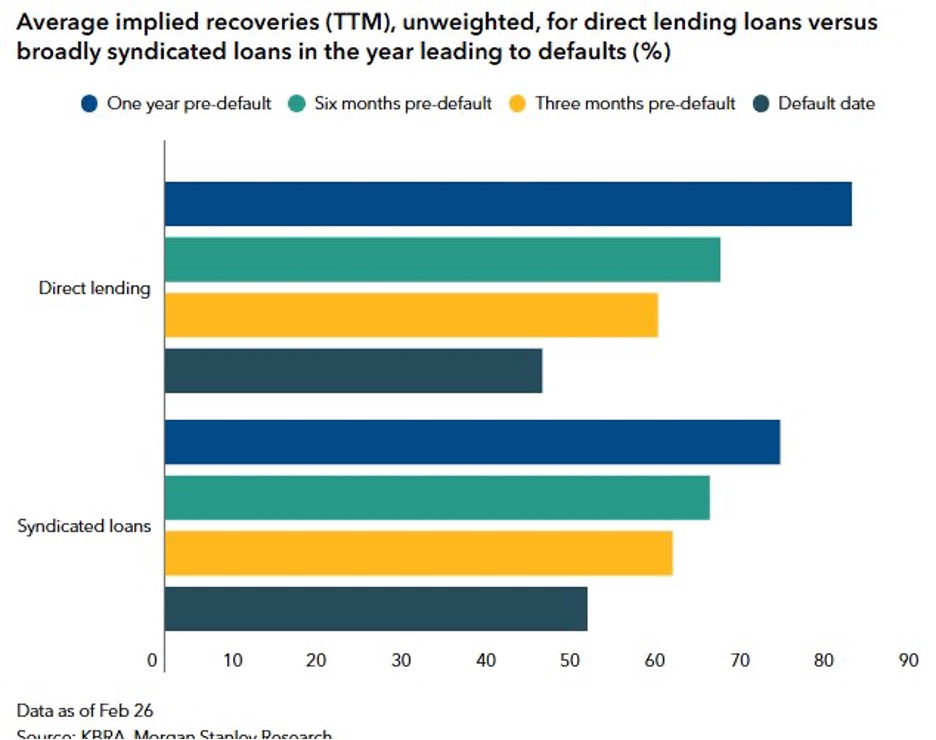

?Q: “How did you go bankrupt?” A: “Two ways. Gradually, then suddenly.” Ernest Hemingway, The Sun Also Rises

The chart below shows the prices of BSL and DL loans one year before default vs. default date. By the default date, direct lending loan recoveries fall below 50 cents, from prices above 80 just one year earlier. Broadly syndicated loans show a similar pattern, declining from the high 70s to just above 50 cents during the same period. The lesson is simple: the longer you wait, the more it costs.

Bottom line: deal with problems early, and the outcome is likely to be better.

The real damage occurs long before the bankruptcy filing. A deteriorating business model, covenant breaches that are not adequately addressed, bad PIK that digs a deeper hole for the issuer, cash burn, and more. Just as Hemingway’s bankrupt character did not wake up broke overnight, companies rarely arrive at distress without warning signs. Deteriorating earnings, shrinking liquidity, customer concentration, margin pressure, management turnover, and excessive leverage are just a few of the key signals that are usually visible well before an out-of-court restructuring or bankruptcy filing.

Proactive, forward-looking asset management plays a critical role in monitoring performance, identifying trends early, and having the discipline and experience to maximize outcomes. Every day, month, and quarter spent ignoring those signals increases the probability of default and decreases recovery value for existing lenders. What could have been a manageable problem may become a much bigger one. For companies that are on plan or ahead of plan, lenders should allow management to operate and let their winners win. But for companies that are falling behind, lenders are well served to have constructive conversations with borrowers and sponsors and take initiatives to help them get back on the right path.

Takeaway #1: Address problems early. The earlier a problem is confronted, the more value can be preserved.

Takeaway #2: Sell before default, if possible.

Takeaway #3: Covenants are important because they force meaningful conversations with the borrower.

Takeaway #4: BSL is liquid credit. Direct lending offers considerably less liquidity, so it is important to be ultra conservative, lending to non-cyclical businesses owned by strong sponsors, with healthy operating margins and cash flow, and the right capital structure.

Takeaway #5: Covenants are rare in BSL, however DL should never give up key covenant protection as this would render asset management somewhat ineffective prior to default.

|

|

Click above to access content To follow Bruce’s thoughts on the markets, investing and more, follow @bruce_markets |

|

|

|

|

|

Exclusive Content |

The New Chapter 11: Get In, Get Out |

|

|

Click above to access content |

Our Take: Twenty years ago, Chapter 11 was largely about fixing companies. Today, as Sunny Singh bluntly observes, it is increasingly about exiting bankruptcy as quickly as possible.

Of course, once a company arrives in court post-LME, post-SPV financing and carrying a cap stack that “looks like a maze,” there is often little left to restructure operationally anyway. The real challenge becomes making it through the case before the liquidity runway disappears.

Perhaps most striking is how casually administrative insolvency is now discussed. The idea that large debtors may simply run out of cash mid-bankruptcy once would have been extraordinary. Apparently not anymore.

Yet, the real canary in the coal mine — bankruptcy fees — still has not entered the conversation. But without addressing the impact of fees, it is hard to see how large-scale restructurings can rehabilitate companies as they did in the past. |

|

|

|

|

|

Advocacy in Action |

A United Front Against the Champerty Bill… |

|

Click above to access content |

Our Take: The CRC joins other industry associations in opposing NYS legislation imposing a champerty defense in sovereign debt restructurings. |

|

|

|

|

|

|

U.S. Special Situations Outlook |

June 11, 2026 |

| Learn More |

|

|

|

Collateral verification in the wake of MFS |

June 17, 2026 |

| Learn More |

|

|

|

|

|

|

|

|

|

|

TMA NYC Joint Pop Up Happy Hour |

June 30, 2026 |

| Learn More |

|

|

|

|

The Data Download |

Bringing Transparency to the Bankruptcy Process |

|

|

|

|

Click Above to Access The Data Download |

Our Take: The Daily Cost of BK Legal fees Are Increasing. Are we shocked? No. We took a deep dive to see what is driving up the daily cost of restructurings and the culprit: Increasing Legal Hourly Rates. We analyzed final fee apps for top debtor law firms from 2018 to 2024 and found average hourly legal fees have increased by over 65% since 2018. Maybe a little bit of sunlight is the right disinfectant to help remedy the problem…. |

|

|

|

|

|

|