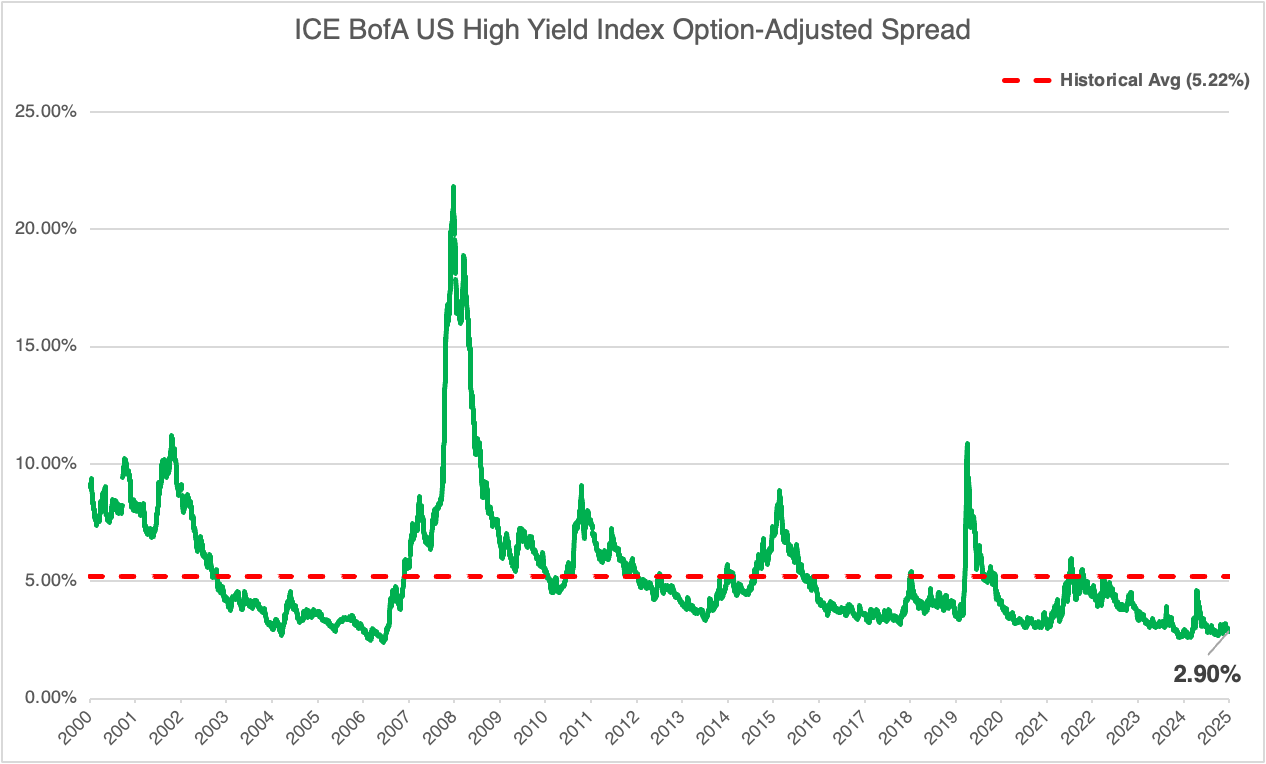

2026 Macro Outlook 1. Credit: Clip your cash flow, remain constructive With rates and equity volatility well contained, financial conditions loose, and earnings trending higher, we will likely see credit spreads remain stable. As a result, credit investors should earn a yield of 6.5% to 7%. High-yield spreads are relatively tight, sitting just inside +300 bps with a yield-to-worst of 6.6% for the HY Master Index. In 2025, BB’s tightened 70 bps while CCC’s widened 70 bps as the up-in-quality theme prevailed. In 2026, I expect HY bonds to trade with lower volatility as spreads grind slightly tighter in the coming months. HY investors may even see spreads tighten to their tightest level this century, touching +250 bps level, not seen since the GFC. The grind tighter combined with active new issuance should enable HY investors to earn their coupon plus 50 bps, or about 7%. Multi-asset public credit is the optimal way to invest across the public credit markets. The greatest risk factors for public credit investors are highlighted in my Top 10 Risk Factor list that I posted yesterday, but top of the list is an economic slowdown or significantly tighter financial conditions which are low probability events this year.

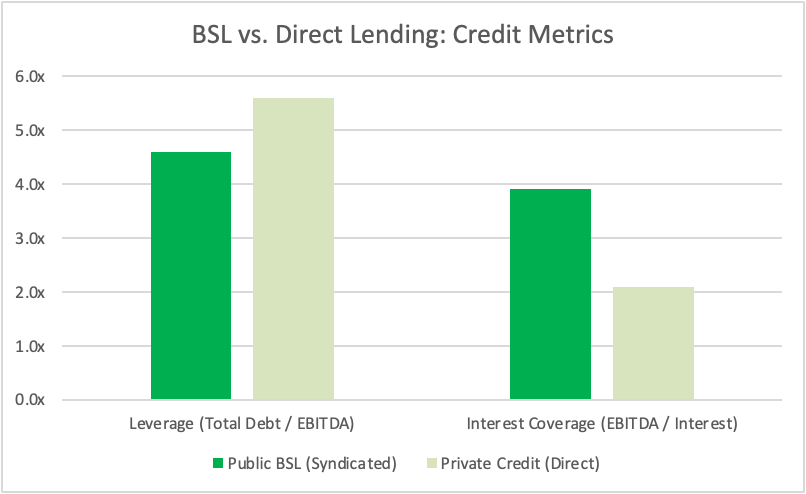

2. Private Credit: Private credit should see a meaningful pickup in deal flow as PE has a banner year for buying/selling companies while asset owners and CapEx accelerate financing plans. This backdrop should keep private credit managers exceptionally busy throughout the year: direct lending, opportunistic credit, and asset-based lending strategies are well positioned to benefit from deal flow and improving credit conditions. Of course, strong sourcing channels and disciplined underwriting standards are key determinates for outcomes. These three core PC strategies should generate returns in the 10–12% range exhibiting materially lower volatility than public markets. Private Credit represents a stable asset class driven by idiosyncratic decisions and outcomes with risk-reward superior to the public debt and equity markets.

3. Rates: Front-end lower, long-end anchored The front end of the curve should continue to rally as the Fed eases policy and maintains purchases of short-term Treasuries. By contrast, longer-dated yields are likely to remain sticky, with the 10-year UST fairly valued in a 4.00%–4.25% range. A meaningful break lower in long rates would likely require the onset of QE program or inflation to settle in at ~2%. A dove will the reins in May who will make it his mission to lower rates in an effort to allow the economy to heat up. Rate volatility should continue to compress: the MOVE index, which has oscillated between 60 and 150 over the past three years, is likely to trade below 50 later this year. I expect the Fed to cut rates three times in 2026, bringing the policy rate towards its neutral level of ~3.0%. The risk to this scenario is higher inflation.

4 . Equities: High valuations, range-bound returns, subdued volatility The S&P 500 enters the year trading at roughly 23.5x forward earnings, an elevated multiple by historical standards. As a result, returns are likely to be more range-bound despite a constructive macro backdrop. I expect the S&P 500 to trade between 6,500 (-5%) and 7,666 (+12%) over the course of 2026. Equity volatility should remain well behaved, with the VIX largely confined to a 10–20 range, likely drifting lower in the coming months. This contrasts sharply with last year, when the VIX spent most of the time between 15–25, spiking above 50 in April. In this environment, volatility-selling strategies are likely to underperform. Earnings growth of ~10% is achievable given continued economic strength, but upside equity returns may be limited given starting valuation levels. The two major risks to this scenario are significantly slower GDP growth and/or AI bubble that bursts.

Conclusion: 2026 is shaping up less as a year for directional conviction and more as a test of portfolio construction discipline. With policy easing expected to be incremental and asset prices already reflecting a benign macro regime, the opportunity set will increasingly favor credit selection over beta. Capital allocators should prepare for an environment where carry, relative value, and structural inefficiencies matter more than broad market exposure, and where resilience to policy or inflation surprises is as important as upside participation. If volatility continues to compress, the real edge may come from building portfolios that can compound steadily, while remaining positioned for regime shifts that markets may be underpricing today. |